Do you ever look at your bank account and wonder, Where does all my money go?

I used to ask myself that same question—every month, like clockwork. I’d start with a decent paycheck, but by the middle of the month, I was down to the bare bones, anxiously waiting for the next payday. If that sounds familiar, stick with me—because I’ve cracked the code. And yes, it involves a little thing called budgeting. Now, before you roll your eyes and imagine a spreadsheet with more boxes than you can count, let me tell you that budgeting doesn’t have to be scary or restrictive. It’s not about taking all the fun out of life or becoming a financial robot (beep beep!). In fact, it’s the opposite! Once I started budgeting, I felt freer—like I was finally in control for the first time.

Here’s how I did it, with a few pro tips sprinkled in for good measure.

目次

Track Every Penny (Yes, Every Single One)

It all started when I realized that I wasn’t actually aware of where my money was going. I thought I had a handle on it, but reality hit hard when I downloaded a budgeting app (I used Mint, but there are plenty of good ones like YNAB). With a few clicks, I could see exactly where my money was slipping away, and boy was it slipping. Spoiler alert: it wasn’t the big expenses; it was the small, sneaky ones that added up—takeout coffee, spontaneous Amazon purchases, and an array of unused subscriptions (that weight loss app I hadn’t opened in months, anyone?)

Here’s a fun fact: Those little purchases that seem so harmless? Yeah, they’re real-time financial termites. They chip away bit by bit until you’re wondering why there’s nothing left but dust (from dust to dust, get it? Anyone? No?) Okay, so that’s where I started—just by tracking every penny. The app did most of the heavy lifting, but you could easily do the same with a notebook (but let’s be real, though no one should still be doing that in the 21st century.)

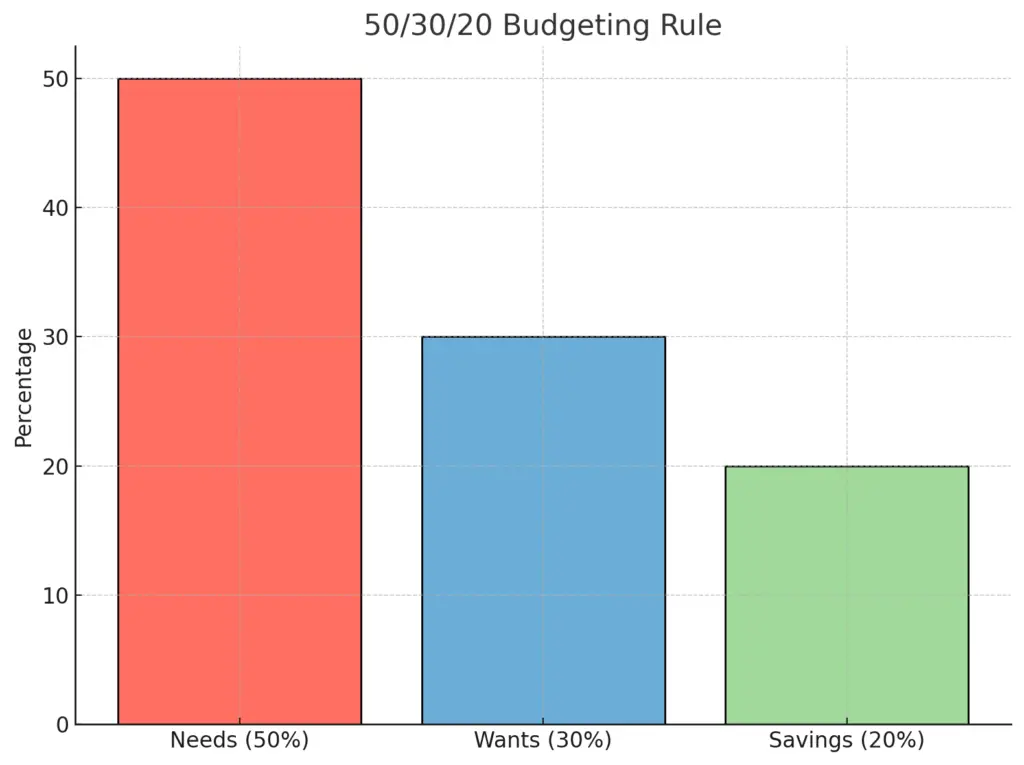

Create a Budget That Works for You

Here’s where things get more interesting. Once I saw where my money was going, I decided to make a plan—a budget. But I didn’t want something rigid or depressing, because hello? life! I needed something flexible. Enter the 50/30/20 rule: 50% of your income goes toward needs (rent, groceries, bills), 30% toward wants (yes, you can still have fun! ), and 20% toward savings and debt repayment.

I adapted this to fit my lifestyle. For example, I live in a city where rent eats up a bit more than 50%, so I adjusted my “wants” category. And guess what? It worked. I felt free. I could go out for dinner or buy that new book I’d been eyeing without guilt because I knew it was all accounted for.

Now I’m not saying it was smooth sailing from day one. I had to tweak things here and there—like realizing I had to give up my third streaming service because I wasn’t watching anything (Sorry, Prime Video), but once I found the right balance, budgeting became second nature.

Automate, Automate, Automate

Another thing I did (one of the best decisions, if I do say so myself) was to automate my savings. You know that saying, “Pay yourself first”? It’s a game changer. I set up automatic transfers to my savings account the moment my paycheck hit. No thinking, no second-guessing. It was out of sight, out of mind.

It felt like a small win every payday—before I even spent a dime, I knew I had already taken care of my future self. And here’s the kicker: once I got into the habit, I didn’t even miss the money. It just became another line item in my budget, no different from rent or groceries.

Pro tip: If you don’t already have a high-yield savings account, get one. I opened an account with Chime (you could also try Ally Bank), and now my savings are not only automatic but also earning a bit of interest on the side. It’s like watching your money quietly grow without any effort.

Don’t Blame the Takeout; It’s the Little Things

There’s always that person who says, “If you didn’t go out to eat so much, you’d be rich by now.” Well maybe, but also maybe not. Because let’s face it: it’s not just that occasional dinner or takeout that’s ruining your finances. It’s mindless spending on things that don’t actually bring you happiness.

Here’s what worked for me: I created a small “treat yourself” budget—$50 a month just for takeout or grabbing lunch at my favorite spot. It’s my guilt-free spending money. Everything else? I evaluate. Do I really need that new gadget, or am I just killing time on my phone and falling into an online shopping rabbit hole?

The 24-hour rule has saved me from countless unnecessary purchases, and here’s what that is- whenever I see something I think I need, I wait 24 hours. It’s that simple. Nine times out of ten, I forget about it or realize I didn’t want it that much after all.

Review, Tweak, and Reward Yourself

The last piece of the puzzle is reviewing your budget regularly. I sit down once a month, take a look at how I did, and make any necessary tweaks. Did I overspend in one area? Maybe I underspent in another. It’s all about being flexible and adjusting as you go. Life happens—sometimes you need to spend more than expected. The key is to not let one bad month derail you.

And don’t forget to reward yourself. When I hit a savings milestone—say, when I reached $1,000 in my emergency fund—I treated myself to a nice dinner. It’s important to celebrate those wins, no matter how small they seem.

Conclusion: Control = Freedom

At the end of the day, budgeting isn’t about restriction—it’s about freedom. Once I figured out where my money was going, made a plan that worked for me, and automated the important stuff, I stopped asking, Where does all my money go? rather, What can I do with the money I’ve saved?

And that, my friends, is a much better question to be asking.

If you’re ready to get started, I recommend downloading a budgeting app like Mint or YNAB, setting up your savings automation, and giving the 50/30/20 rule a try. Trust me—future you will thank you!

Key Takeaways

Budgeting is less about rules and more about building a life you control, not one controlled by your bank balance. Here’s the vibe:

- Your Money Has a Trail—Follow It: Start tracking every penny, because those small, sneaky expenses? They add up fast. Awareness is power.

- Flexibility is Key: Budgeting isn’t one-size-fits-all. Whether it’s the 50/30/20 rule or your own remix, find a balance that feels sustainable and lets you live guilt-free.

- Set It and Forget It: Automating your savings isn’t just smart—it’s stress-free. Treat it like paying rent, but this time, you’re paying future you.

- Small Tweaks, Big Wins: Every month is a chance to refine. Budgeting isn’t static, and celebrating even small wins can keep the motivation alive.

Remember, it’s not about depriving yourself—it’s about choosing how you want to live, one intentional decision at a time. You’ve got this!